The full form of GST is Goods and Services Tax. It is a comprehensive indirect tax levied on the supply of goods/ services in India. GST was introduced in India on July 1, 2017, and replaced multiple indirect taxes like excise duty, service tax, VAT, and others.

Now let’s see how the GST in India works:

- Tax Structure

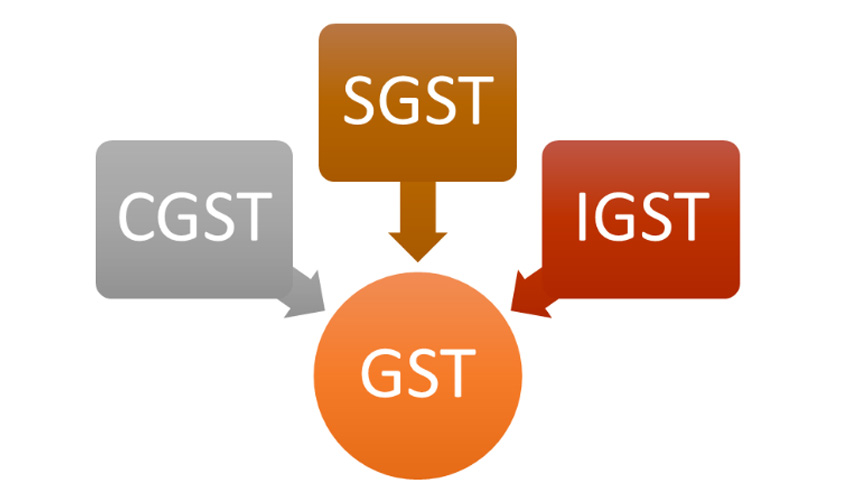

GST in India has a dual structure, comprising the Central Goods and Services Tax (CGST) levied by the central government and the State Goods and Services Tax (SGST) levied by the state governments. Additionally, there is an Integrated Goods and Services Tax (IGST) applicable to interstate supplies and imports/exports.

- Taxable Event

The GST in India is applied to all the supply of goods/services. The supply could be in any form such as sale, transfer, barter, exchange, rental, lease or importation of goods and services made during business.

- Business Registration:

Businesses with a turnover of more than the prescribed threshold are required to register under GST is mandatory. During registration, businesses are issued a unique Goods and Services Tax Identification Number (GSTIN).

- Tax Rates:

The GST in India has different tax rates for different goods/services. The rates are categorized into four main slabs: 5%, 12%, 18%, and 28%. Some essential items like food grains, books and healthcare services may be exempt or subject to a lower rate of tax.

- Input Tax Credit (ITC):

One of the benefits of GST is the availability of input tax credits. Businesses can claim credit for the GST paid on their purchases or inputs. This credit can be utilized to offset the GST liability on their outward supplies. It helps in avoiding the cascading effect of taxes and promotes the concept of “tax on value addition.”

- Return Filing

Registered businesses are required to file regular GST returns to report their inward and outward supplies and calculate their tax liability. The returns can be filed online through the Goods and Services Tax Network (GSTN) portal. Various types of returns are applicable based on the nature of the taxpayer’s business.

- Compliance & Enforcement

GST in India is supported by a robust technology infrastructure that tracks transactions, minimizes tax evasion and ensures compliance. Businesses are required to maintain proper records, issue tax invoices and comply with GST regulations.

Types of GST in India

There are primarily three types of GST in India. Let’s have a look at them:

1. Central Goods and Services Tax (CGST):

- CGST is levied on the intra-state supply of goods/ services by the central government.

- CGST is governed by the Central Goods and Services Tax Act of 2017.

- The revenue which is generated from CGST is retained by the central government.

2. State Goods and Services Tax (SGST):

- SGST is levied on the intra-state supply of goods and services by the state governments.

- Governed by the respective State Goods and Services Tax Act of each state.

- The revenue generated from SGST is retained by the state government where the supply occurs.

3. Integrated Goods and Services Tax (IGST):

- IGST is the tax levied on the inter-state supply of goods/ services by the central government

- It is governed by the Integrated Goods and Services Tax Act of 2017.

- The revenue generated from IGST is shared between the central and state governments based on the prescribed formula.

History Of GST in India

The implementation of the Goods and Services Tax (GST) in India on July 1, 2017, was the culmination of a lengthy process that began years earlier. A committee was set up by then Prime Minister Atal Bihari Vajpayee to draft the GST law, and the new tax regime groundwork was laid in 2000. In 2004, a task force recommended the implementation of the GST to enhance the existing tax structure.

In 2006, the Finance Minister proposed the introduction of GST on April 1, 2010. Subsequently, in 2011, the Constitution Amendment Bill was passed to enable the implementation of the GST law. The Standing Committee began discussions on GST in 2012 and presented its report on GST the following year. However, the implementation of the law faced delays as it was not passed in the Rajya Sabha.

Progress was made in 2014 when the new Finance Minister, Arun Jaitley, reintroduced the GST bill in Parliament. The bill was passed in the Lok Sabha in 2015 but encountered further obstacles in the Rajya Sabha.

Finally, in 2016, the GST was given the green light, and the amended model GST law was passed in both houses of Parliament. After that, it received the assent of the President of India. In 2017, four supplementary GST Bills were passed in the Lok Sabha, followed by their approval by the Cabinet. The Rajya Sabha also passed these four supplementary GST Bills, paving the way for the implementation of the new tax regime on July 1, 2017.

Tax Laws Before the Implementation of GST

- Each state in India had its unique tax regime, leading to variations in tax systems across the country. The tax collection was separate for the central and state governments on the goods/services.

- The burden of import taxes was often transferred to individuals other than the actual importer, resulting in an indirect impact on different individuals. In the case of direct taxes, the taxpayer was responsible for paying the tax.

- Earlier GST in India had a combination of direct and indirect taxes in place before the introduction of GST.

Objectives of implementing GST in India

The objectives of implementing GST in India to benefit businesses and individuals by:

- Streamlining tax structure and simplifying compliance

- Creating a unified market and promoting seamless trade

- Eliminating tax cascading and promoting efficiency

- Boosting competitiveness and ease of doing business

- Enhancing tax administration and reducing evasion

- Ensuring transparency and accountability in the tax regime

Advantages of GST

Having a GST basic knowledge will unlock your potential to several advantages of GST for the economy and businesses like simplifying the tax structure, promoting economic growth, enhancing competitiveness, improving tax compliance, etc.

Let’s look at some of the benefits of GST in detail:

- GST replaces multiple indirect taxes with a single unified tax system, simplifying tax compliance and administration.

- GST allows for input tax credits, eliminating the cascading effect of taxes and reducing the tax burden on businesses. Thus this promotes efficiency and reduces the cost of goods and services.

- GST in India creates a common market across the country enabling the seamless movement of goods and services and promoting trade without inter-state barriers.

- One of the advantages of GST is it reduces logistics costs, improves supply chain efficiency and enhances the ease of doing business, making Indian goods/services more competitive in the domestic and global markets.

- GST promotes transparency and accountability in tax transactions and reduces tax evasion via the use of digital systems and robust tracking mechanisms.

- GST in India has simplified the tax filing process with the help of a unified online platform thus helping in reducing paperwork and making it easier for businesses to comply with tax regulations.

- By attracting investment, promoting entrepreneurship and creating a favourable business environment the GST is expected to boost economic growth.

- GST aims to bring down the overall tax burden on individuals/customers/consumers by reducing the prices of goods/services and making them more affordable.

Who Should Register for GST?

It is important for entities and individuals to register for GST and get GST basic knowledge:

- E-commerce aggregators like Amazon, Shopify, eBay, Etsy, etc.

- Suppliers who supply through E-commerce aggregators

- As per the reverse charge mechanism, Individuals who pay taxes

- Agents of input service distributors and suppliers

- Non-Resident individuals who pay GST

- Businesses that have a turnover that is more than the prescribed threshold limit

- Individuals who registered before the GST law was introduced in India

How to do Registration for GST

Under GST system in India, eligible companies must register themselves on the government’s GST portal to obtain a unique registration number known as Goods and Services Tax Identification Number (GSTIN) and get GST details.

Registration is mandatory for service providers, buyers, and sellers. Businesses earning a total income of INR 20 lakhs or more in a financial year are required to register for the GST. This registration process typically takes 2-6 working days to complete.

Know the GSTIN – GST Identification Number

It is important to have basic GST knowledge like knowing all about the GSTIN.

GSTIN is a unique 15-digit code assigned to taxpayers, customized according to their state of residence and PAN, serving multiple essential purposes.

- Availing of Loans becomes easy with the help of this number

- Ease to claim the refunds

- Provides ease in the verification process

- Corrections can be made easily

You can also verify your GST Number online from the official site here and get GST details

GST Registration Certificate:

A GST Certificate is an important legal document issued by the relevant authorities to companies registered under the GST system. To be eligible for registration, businesses with an annual revenue of at least Rs. 20 lakh and certain specialized enterprises must apply. The GST registration certificate, issued through Form GST REG-06, can be downloaded from the official GST Portal.

Unlike physical copies, the certificate is available in digital format only. It has important details like GSTIN, Legal Name, Trade Name, Business Constitution, Address, Validity Period, Types of Registration, Specifications of the Approving GST Officer and Date, etc. and get all the GST information here

GST Returns

GST Returns are essential documents that taxpayers must file to report their income to the authorities and determine their tax liability. Under the Goods and Services Tax system, registered dealers are required to submit their GST returns, providing information on purchases, sales, input tax credit, and output GST. Businesses typically need to file two monthly returns and one annual return. These returns play a crucial role in ensuring compliance with GST regulations and maintaining accurate financial records.

GST Rates

The GST Council has categorized goods and services into different GST rates. Some products are exempt from GST, while others are subject to 5%, 12%, 18%, or 28% GST. Since the introduction of the new tax regime in July 2017, there have been several revisions to the GST rates for various goods and services. These changes ensure a fair and balanced taxation system while accommodating economic and policy considerations.

How do I Calculate GST?

Calculating the GST amount for filing returns can be a complex task, considering various factors like ITC, exempted supplies, reverse charges, and more. It is crucial to accurately determine and pay the correct GST amount to avoid any penalties. Failure to pay the full GST amount may result in an 18% interest charge on the shortfall. Therefore, it is essential to diligently ensure the accuracy of GST payments to maintain compliance and avoid unnecessary financial burdens.

Apart from this, there are GST calculators available online which can help taxpayers to calculate GST easily by inputting all the necessary details related to the business.

To get a basic knowledge of GST let’s look at the example below:

| Description | Amount (INR) | GST Rate | GST Amount (INR) |

| Taxable Goods/Services | 10,000 | 18% | 1,800 |

| Input Tax Credit (ITC) | -500 | – | – |

| Exempted Supplies | -2,000 | – | – |

| Reverse Charge | 1,000 | 12% | 120 |

| Total | 8,500 | 1,920 |

- The taxable goods/services have a value of INR 10,000 with a GST rate of 18%, resulting in a GST amount of INR 1,800.

- Input Tax Credit (ITC) of INR 500 is deducted from the GST liability.

- Exempted supplies worth INR 2,000 are not subject to GST.

- The reverse charge applies to a service valued at 1,000 INR, with a GST rate of 12%, resulting in a GST amount of INR 120

- The total GST liability is calculated as INR (1,800- 500 + 120)= INR 1,920

GST Payments

Monthly GST payments are now mandatory. Taxpayers are required to file GSTR-1 and GSTR-3B forms. In cases where refunds are applicable, relevant forms need to be submitted. GST payments can be made either via online or offline mode. And once the payment is completed, it is necessary to generate a challan as proof of payment.

GST E-Way Bill

The e-Way bill is a digital document generated to provide evidence of goods movement. It can be conveniently generated from the GST portal, serving as proof for transportation purposes.

GST Changes According to Union Budget 2023-2024

Here are the key changes in Goods and Services Tax (GST) announced in the Union Budget 2023-2024 by Finance Minister Nirmala Sitharaman.

- Section 10 amended: The composition scheme can now be availed by taxpayers who supply goods through e-commerce operators.

- Section 16 amended: If a recipient taxpayer fails to pay the supplier’s invoice value along with GST within 180 days from the date of invoice issuance, they are liable to pay the value along with compounded interest as per Section 50.

- Sections 37, 39, 44 and 52 amended: Taxpayers are now restricted from filing GSTR-1, GSTR-3B, GSTR-9 and GSTR-8 after 3 years from the due date of the respective tax period.

- The E-commerce operator will be charged INR 10,000 or the tax amount equivalent, whichever is higher in the below-given cases:

– If an unregistered person is allowed to sell goods/services or both via these operators. Excluding the cases where the person/ business is exempted from GST.

– Allowing inter-state supply of goods/services through registered persons whereas they are ineligible for it.

– If the person is exempted from GST registration and even do not provide authentic details in the GSTR-8 of goods sold by the people. - Decriminalization of the following offences:

– As per the CGST Act, an officer is prevented from discharge of duties by a person

– If material evidence and documents are tempered by the person

– Either the person fails or provides false GST information under CGST Act and Rule - Limits have changed in between 25-100% of the tax involved regarding the compounding offences.

- Section 158A has been inserted in the CGST Act to enable businesses to share GST data with digital consent. This section outlines the manner and conditions for sharing information as declared by the registered person on the portal.

– Outward supplies statement

– Registration application

– Returns filled under GSTR-1, 3B or 9

– Generation of e-bill or e-invoice or any other details.