What is the full form of GST?

Taxes are major sources of revenue for the government for the functioning of a country. The Goods and Services Tax (GST) Act was passed on 29th March 2017 and came into effect on 1st July 2017

GST full form is Goods and Services Tax. It is a mandate tax charged by Central Government. The tax is levied under the goods and services taxable under the GST system in India. The government uses that money for the functioning and administration of the nation. Every individual who is adding value to the supply chain will have to pay GST. GST in India is a form of indirect tax for the entire country.

What is the full form of GST and list it’s various types

GST in India has four types. The types of GST are CGST, SGST, IGST, and UTGST.

Each type has different taxation rates applicable at the buyer’s end. Let’s understand this quickly and easily:

- CSGT: CSGT is an abbreviation for Central Goods and Services Tax. It is levied on the intra-state movement of goods and services by the central government.

- SGST: State Goods and Services Tax also known as SGST. It is levied by the state government on the intra-state supply of goods and services, except for alcoholic liquor. It is charged solely on the product’s transactional value- an amount the buyer needs to pay. SGST may vary as per the state. One tax, one nation is the objective of SGST.

- IGST: Full form of IGST is Integrated Goods and Services Tax. It is levied on the inter-state supply of goods and services by the central government. It is charged on the import of goods. The central government collects all the tax in the form of IGST and distributes it amongst various states.

- UTGST: Union Territory of Goods and Services Tax is a full form of UTGST. The government levied a tax on the supply of goods and services in the Union Territories of the country. Along with UTGST the CGST is also charged on this. Andaman and Nicobar Island, Lakshadweep, Chandigarh etc. are Union Territories.

What commodities are not subject to GST

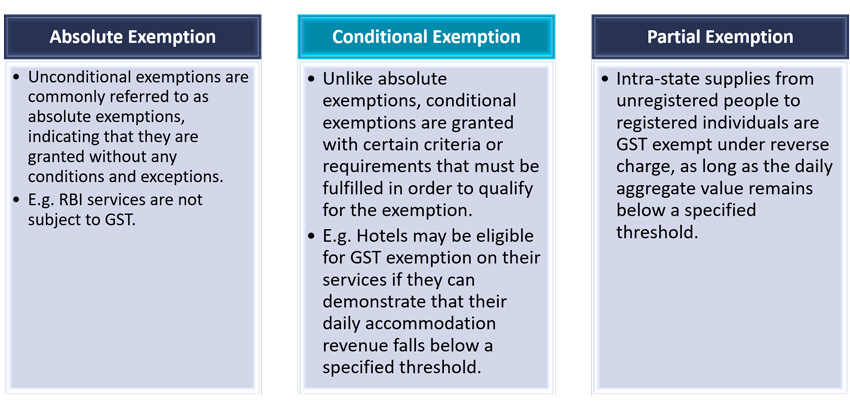

GST in India is exempted on various factors and goods, services, supplies, businesses and individuals must register to GST provided they have certain conditions. The GST exemptions in India are bifurcated into three types:

Supplies exempt under GST:

Supplies exempted from GST may fall under one of the following three categories:

- Taxable supplies under NIL rate of tax (i.e. 0% tax rate)

- Supplies which are either of both i.e. partially or wholly exempted from IGST or CGST as per the amendment to Section 11 of the CGST Act or Section 6 of the IGST Act

- Supplies which are ‘Non-taxable’ as defined under Section 2(78) of the CGST Act (e.g. alcohol for human consumption)

Remember, NIL-rate supplies are not as same as Zero-rated supplies.

To understand this better, let’s examine the differences between Exempt, Nil-Rated, Zero-Rated and Non-GST Supplies.

| Supply type | Description |

| Exempt | The supply is taxable but, GST is not applicable here. Input Credit Tax (ICT) cannot be claimed |

| Nil-rated | Supplies to which whose GST rate is set at 0% e.g. salt and grains |

| Zero-rated | Export supplies, goods or services provided to SEZs or SEZ developers. |

| Non-GST | Supplies that do not come under the scope of GST laws. E.g. alcohol for human consumption. |

GST Exemptions:

Let’s look at the list of items, businesses and taxpayers who can avail of tax exemption under the Goods and Services Tax regime.

GST exemption from registration:

The following taxpayers need not register for GST:

- Individuals belonging to the threshold exemption limit

- Exempt suppliers of goods and services

- Individuals supplying Non-GST goods and services

- Agriculturists

- Individuals supplying goods with a reverse charge

GST exemption for start-ups and small businesses:

- Any business whose turnover is less than INR 40 Lakhs is exempted from GST

- Companies which has an annual aggregate turnover of less than 1.5 crores can avail of a composition scheme under GST. Depending on the turnover amount allows individuals to pay taxes at a fixed rate. This rate may vary between 1-6%

- Small businesses are exempted from e-invoicing under GST. However, businesses with a turnover of more than INR 50 crores have to apply for e-invoicing mandatorily.

- Small businesses earning less than INR 5 crores have the option to file their taxes on a quarterly basis.

Goods exempted under GST:

- Fresh and dry vegetables

- Non-GST goods like fish, eggs, fresh milk, etc.

- Grapes, melons, ginger, garlic, unroasted coffee beans, green tea leaves that are not processed, and more.

- Food items that are not put into branded containers like rice, hulled cereal grains, wheat, corn, etc.

- Components like Human blood

- Jute fibres, raw silk, khadi fibre, etc. which are unspun

- Hearing aid manufacturing parts, chalks, slates, handloom, etc.

Note: Certain non-GST items, once processed, will attract a GST.

Services exempted under GST:

- Most agricultural services, such as harvesting, packaging, warehousing, cultivation, supply, and machinery leasing, are exempt from GST. However, the rearing of horses is an exception to these exempted services.

- Public transportation services e.g. auto rickshaw, metro, metered cabs, etc.

- Transportation of agricultural goods and services outside India

- Labour supply for farms

- Goods transportation charges less than INR 1500

- Retail packing, free conditioning, waxing, etc.

- Foreign diplomatic and government services

- Healthcare and education services

- Services offered by the RBI, the IRDAI, the Central and State Governments, the NPS, etc.

- Different banking services

What is the full form of GST in Tax and explain the workability of GST

The Goods and Services Tax (GST) in India is a comprehensive, multi-stage, destination-based tax which is applied to the value added at each stage of the supply chain. GST in India is a unified domestic indirect tax law that covers the entire country.

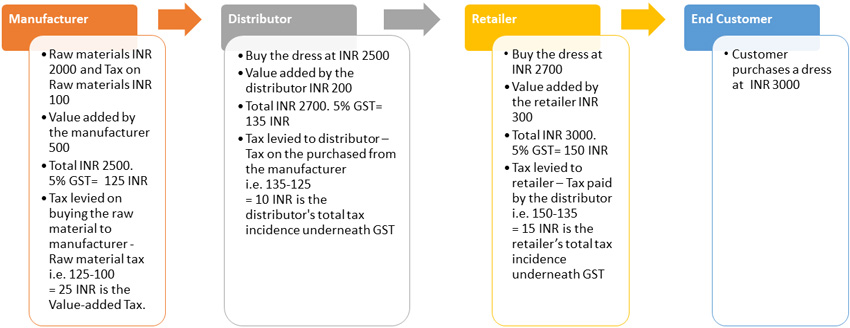

Let’s understand how GST works from the manufacturer to the end consumer with an example and stage-wise:

Stage 1: Manufacturer

The manufacturer buys raw materials for a dress worth INR 2000 and INR 100 as a Tax. The manufacturer added a value of 500 INR to represent the cost or value of the dress. Hence, the total value of the dress is 2000+500=2500. Let’s assume the GST rate on the dress is 5% so, 5% of 2500 is 125 INR

Now, the manufacturer can set off with the tax he paid for the raw material INR 100. Hence the applicable GST will only be INR 25 i.e. (125-100=25). This makes GST a value-added tax.

Stage 2: Distributor

Here, the goods i.e. dress is given to the distributor. The distributor buys the same dress for INR 2500 and adds a value of INR 200. Hence, now the value of the dress is INR 2700 (2500+200). Under GST in India, he will pay 5% which will be 135 INR. This will be set against the tax on the purchased dress from the manufacturer, which is 125 INR. The distributor’s total tax incidence underneath GST will be 135-125= 10 INR.

Stage 3: Retailer

At this stage, the retailer gets the goods i.e. dress from the distributor. Now the retailer adds his margin of INR 300 for purchasing a dress. The total cost of the dress will be 3000 INR (2700+300). Assuming the GST is 5%, the retailer will have to pay a tax of INR 150 which he can set off against 135 INR tax paid by the distributor. The tax incidence underneath GST on the vendor will be 15 INR (150-135).

Stage 4: Customer

The final price for the dress will be INR 3000

GST is a value-added tax system that enables input tax credits at each stage of the supply chain, except for the final consumer stage. Hence, it is right that GST is one nation, one tax offering financial advantages to traders and businesses.

Why has GST been Introduced in India?

GST in India was implemented to reduce the taxes levied by the central and state governments and simplify the tax system. One Nation, One Tax is the primary concept of the GST regime in India. GST in India was introduced to bring consistency to the tax system. Hence, each state has a fixed and uniform tax structure making it easier for consumers to understand taxes. The GST system in India has reduced the likelihood of corruption. However, the primary and most important reason for establishing the GST system is to eliminate the cascading effects of taxes.

Cascading Effect of Taxes – The cascading effect of taxes refers to the situation where a product is taxed at multiple stages of its sale, leading to repetitive taxation. Each stage incurs a tax on top of the previous one, causing the end consumer to bear the burden of “tax on tax” already paid. In order to prevent this repetitive taxation, the government implemented the Goods and Services Tax (GST) as a unified tax to be paid by the entire nation. This move aimed to eliminate the cascading effect and ensure a more efficient and fair taxation system.

Are there any benefits of GST?

Yes, indeed there are. Here are some of the benefits of GST

- One of the major benefits of GST is that it has eliminated the cascading effects of taxes by requiring consumers to pay only one tax, bringing uniformity and simplification to the tax collection process.

- Since the cascading effect is out of the scenario the prices of goods and services have significantly lowered.

- Business owners and service providers with a turnover of less than 20 Lakhs INR or less will not have to pay GST as per the Indian government.

- The practice of selling goods and services with receipts to the customers has eliminated corruption.

- Online GST registration and GST returns have made tax filing much easy.

- Small businesses benefit from the GST implementation because they only have to pay one tax.

- Small businesses with a turnover of up to INR 75 lakhs can avail of GST benefits through composition schemes, paying only 1% of their turnover.

- GST implementation has enhanced accountability and transparency in India’s unorganized sectors. It has introduced new compliances and facilitated online payments in these sectors.

Conclusion

The cascading effect of taxes refers to the situation where a product is taxed at multiple stages of its sale, leading to repetitive taxation. Each stage incurs a tax on top of the previous one, causing the end consumer to bear the burden of “tax on tax” already paid. To prevent this repetitive taxation, the government implemented the GST in India as a unified tax to be paid by the entire nation. This move aimed to eliminate the cascading effect and ensure a more efficient and fair taxation system. In conclusion, the Goods and Services Tax (GST) has marked a significant milestone in India’s taxation history. Since its implementation in July 2017, GST has aimed to simplify the tax structure, create a unified market, expand the tax base, and enhance compliance and transparency. While there have been challenges during the initial phase of implementation, the government has actively addressed concerns and made necessary adjustments. GST has not only boosted revenue collection but also fostered a more efficient and equitable tax system. As India continues to evolve under the GST regime, it is expected to further contribute to the country’s economic growth, ease of doing business, and overall development in the years to come.

To learn more about GST sign up here.